Taking action to reduce hail losses

0 July 4, 2014 at 2:36 pm by Glenn McGillivrayFrom an insurance perspective, essentially all of the large-loss hail events recorded in Canada have occurred in Alberta. Indeed, the top three most expensive hailers on record took place in that province.

Emergency Preparedness Canada’s website lists the September 7, 1991 Calgary event as the most expensive hailstorm in Canadian history with $237 million in personal property damage. However, that event was eclipsed by a July 12, 2010 Calgary storm that pelted the city with hailstones of almost four-centimetres in width, resulting in more than $400 million in claims. That storm, in turn, was overshadowed by the August 12, 2012 hailer that saw parts of Calgary pelted with golf ball-sized stones. Insured damage from that event exceeds $500 million.

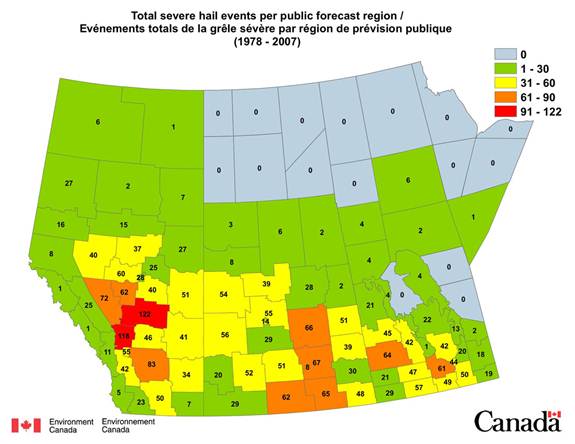

These numbers may lull one into believing that damaging hailstorms can only happen in Alberta. However, hail can effect every province and territory in Canada and, historically, has to some degree or another. However, as the map indicates, the majority of hail days in Canada occur in Alberta, the southern Prairies and southern Ontario.

Hail claims for homes and cars are often to repair damage that is only cosmetic – or aesthetic – in nature. However, large hail events often result in claims for replacement of badly damaged roofs which no longer function properly; shredded and missing siding, broken windows and skylights – all of which can allow water into a home; and replacement of auto glass needed to restore the driveability of a vehicle.

Hailstones generally become destructive when they are one inch wide or larger. Once they reach that size, they have the capability to cause extensive damage to industrial and commercial assets; public infrastructure; trees, vegetation, crops and lifestock; vehicles; and, homes.

Some of the measures that can be taken to protect homes against hail have become clearer and better understood in recent years, thanks greatly to more and larger damage and insurance claims surveys conducted on-site after major hail events, and to increasingly more laboratory tests, like those conducted by the Institute for Business and Home Safety (IBHS). Better understanding, however, does not necessarily translate into increased ease of implementation of mitigation measures, thanks to a host of issues, not least of which is openness and acceptance by homeowners and insurance companies.

Though damage to vehicles must also be considered, the answers there are less clear and require further investigation.

Housing

A quick look at the data available on recent hailstorms in Alberta indicates that while the number of damaged vehicles is substantial when large hail falls, damage to houses is equally as frequent. The data also indicates that the average hail claim is roughly twice as much for a home than for a vehicle.

Much of the discussion around mitigation of hail damage centres around use of impact resistant (IR) roofing products.

As is true in the U.S., the majority of homes in Canada use asphalt shingles for roof covering. According to www.roofery.com “Asphalt shingles can be categorized in terms of design types and constitutive elements. They can also be categorized depending on their weight, mat thickness, and type of filler materials. It continues: “Asphalt shingle ratings have been formulated by the American Society for Testing and Materials (ASTM). ASTM has set standards for both fiberglass and organic varieties of shingles.

Fiberglass shingles with an ASTM D 3462 certification and organic shingles with ASTM D 225 certification comply with ASTM standards. To be certified to these standards, the shingle products must have successfully withstood procedures such as nail-withdrawing and tear strength tests. Asphalt shingle ratings cover criteria such as fire and wind impact resistance. Fiberglass shingles are normally Class A rated (the highest fire resistance), and organic shingles are usually Class C (the lowest fire resistance).

Impact resistance relates to wind damage and those shingles with a Class 4 rating have extra adhesive strips under the tabs which make them the most wind resistant. They also take six nails as opposed to the usual four to fasten them in order to increase their wind resistance. The Underwriters Laboratory (UL) test specifically tests against wind and hail impact. Only on withstanding 60 miles per hour winds for two hours will shingles win the UL certification. As for hail ratings, the shingles have to remain unscathed under a barrage of steel balls simulating hail stones. Consumers can check for the ASTM and UL labels on shingle packaging and in product brochures.”

According to CASMA – the Canadian Asphalt Shingle Manufacturers’ Association – hail can have two main effects on asphalt roofing: aesthetic and functional: “By far the most common type of damage caused by hail [is aesthetic]; small localized areas with minor loss of granules. This type of damage generally has little impact on the expected life of the roof. Functional damage is where there is sufficient damage to the shingles to either cause a short term leak or to reduce the life of the roof. This type of damage is recognized by significant granule loss (easily visible from the ground, large areas of asphalt becoming exposed) or shingle fracture/penetration which can be seen by fractures through the back of the shingle. Generally shingle replacement is only required in severe cases of damage. Remember that asphalt shingle applications provide at least two layers of shingle material over the entire roof.”

ASTM standards are not typically used by Canadian shingle manufacturers whose products are not exported to the U.S. and, thus, are usually only used for shingles that are manufactured in the United States for use there, or that are imported into Canada. For an impact resistant (IR) roofing standard that is used by both U.S. and Canadian shingle manufacturers one must look to Underwriters Laboratories standard UL 2218 Impact resistance of roofing systems, which is the recognized norm for asphalt roofing regularly used in both countries.

According to Tampa-based IBHS “UL 2218 is a test that is administered by Underwriters Laboratories and involves dropping steel balls of varying sizes from heights designed to simulate the energy of falling hailstones. Class 4 indicates that the product was still functional after being struck twice in the same spot by 2″ steel balls. Note that this standard is appropriate for flexible roofing products like asphalt shingles, and metal panels or shingles.”

It has been found that asphalt shingles designated as Class 4 under the UL standard hold up very well against 95 per cent of all hailstorms experienced. Thus, it is highly recommended that insurers replacing a hail-damaged roof, particularly in areas that regularly experience significant hail events, should make it their policy to only provide reimbursement for Class 4 IR roofing that meets UL 2218. The moderately higher cost over installation of a Class 1 shingle would be small given the potential claims savings, and could be reduced by an insurer’s buying power.

Worthy of consideration is the idea that new home builders use a Class 4 shingle whenever a home is being built in a high-risk hail zone, such as in southern Alberta and southern Saskatchewan. Other considerations include use of roof systems other than asphalt, such as metal and plastic.

In moderate hailstorms, it is often just the roof of a home that is damaged. However in larger, very destructive storms, the experience in Texas and elsewhere is that while roughly half the damage is related to the roof, the other half is related to siding, vents, soffits, fascia, skylights and fenestration (i.e. windows and doors). To-date, while a significant amount of research has been conducted on roofing systems, very little has been done on these other items, which can prove to be significant sources of damage. There is a huge void in the science and testing, and virtually no IR standards exist for siding, vents, soffits, fasica and fenestration. One consideration is to encourage use of cement board over aluminum or vinyl siding, particularly in high-risk hail zones. An additional benefit to cement board is it’s higher resilience to fire, which makes it suitable for use in the wildland urban interface (WUI) where risk of damage/loss to wildfire is greatest.

Clearly, much more work needs to be done in the testing of siding, vents, soffits, fascia, fenestration etc., and in the development of IR standards for same..

Vehicles

When it comes to protection of vehicles against hailstorms, the simplest and most common form of mitigation is to get vehicles under cover prior to a storm. Such cover can be permanent – as with car ports and garages; or temporary, as with fabric shade systems used to shelter open lot vehicle inventories like those found at car rental lots and auto dealerships. Permanent car port-type structures can take various shapes and forms, and range from being very basic to quite complex in design. One may see various styles and types of permanent car ports while driving through the Dallas-Fort Worth area.

Keeping cars under permanent cover provides ideal protection. However when use of permanent structures is not possible, temporary tent-like fabric covered structures, as well as custom car covers or blankets such as the type used by owners of vintage cars, may be considered as alternatives. Though there are several manufactures and sellers of car covers/blankets purported to be ‘hail resistant’, to-date, it is unclear if any have been subjected to rigorous hail testing, and currently no standards bodies have published standards for such products. Several companies in the United States manufacture and market fabric structures to protect vehicles against hailstones, as well as against the sun’s harmful UV rays. Such structures can be seen at rental car lots (for instance, at the Dallas-Fort Worth Airport), auto manufacturing plants and car dealerships.

In such places as Texas, it is common for car dealerships to be incentivized through their insurance companies to use such covers. Incentivizing the use of vehicle covers – whether permanent or temporary – is easily done for insureds who hold large inventories of vehicles. However, it may not be possible, realistic or desirable to incentivize property owners to provide such cover if the vehicles they protect are not their own, as with public parking lots or employee parking lots, for example. This represents a big gap that would be difficult to address.

Perhaps more consideration may need to be put into rigorously testing and issuing a standard for custom car covers/blankets.

Conclusion

The need to address the problem of mounting hail-related claims in Canada could not be more acute, as the industry will likely see more hail damage in Canada going forward. This, not necessarily because of any projected increase in frequency of hail, but due to increased concentration of values and growing costs of replacing damaged property in such places as Calgary.

Large gaps currently exist in the testing of siding, vents, soffits, fascia, fenestration etc. as well as with the implementation of IR standards for same.

There are also clear gaps that need to be filled regarding research to better protect vehicles from large and damaging hail.

This being said, it is likely best for the Canadian insurance industry to concentrate first on those measures that make the most sense, where we have the most knowledge, and where insurers will get the best return – on roofing.

Currently, we know enough to be able to say that IR roofing products perform markedly better than non-IR products. As a result, insurers writing business in high-risk hail zones need to consider leveraging their buying power, and incentivizing their use.

The next discussion, perhaps, needs to centre around a push for IR requirements in building codes for homes being constructed in high-risk hail zones.

There are gaps in the research to be sure, however we know enough at this stage to be able to move forward with a plan to better utilize IR roofing products, and we know enough about where research and testing is lacking to begin to work towards filling these gaps.

If not, Canadian insurers writing personal lines business in hail hazard areas should get used to writing big cheques more often.

Note: By submitting your comments you acknowledge that insBlogs has the right to reproduce, broadcast and publicize those comments or any part thereof in any manner whatsoever. Please note that due to the volume of e-mails we receive, not all comments will be published and those that are published will not be edited. However, all will be carefully read, considered and appreciated.

Leave a Reply