‘Taking the comprehensive’ off home insurance

0 December 10, 2015 at 11:40 am by Glenn McGillivray In an age where losses from severe weather are driving changes to homeowners’ policies that are not always seen as positive to insureds, it might be time to think about giving homeowners the option of a cheaper insurance product that limits covers for such things as roof damage from hail.

In an age where losses from severe weather are driving changes to homeowners’ policies that are not always seen as positive to insureds, it might be time to think about giving homeowners the option of a cheaper insurance product that limits covers for such things as roof damage from hail.

In an October 21 piece in Canadian Underwriter Online, I was quoted as saying that hail-resistant roofing should be added to Canadian building codes. My article was based on remarks I had made at AIR’s Toronto Conference the day before.

As a direct result of this report, I soon received two emails from providers of hail-resistant roofing products agreeing with my statement that impact resistant (IR) roofing should be included in building codes and offering assistance in any efforts to make this happen. One email was from the manufacturer of composite rubber roofing (more on that another day) and the other from the manufacturer of steel for metal roofing.

And therein lies the issue.

Numerous roofing products have passed the Underwriters Laboratories 2218 Standard for Impact Resistance of Prepared Roof Covering Materials test, in which a large ball bearing is twice dropped at height onto the same spot on a product. The product can be considered a Class 4 IR product if the resulting damage is only cosmetic – and not functional – in nature (i.e. when the damage is not bad enough to allow water to seep into the structure). Products that have passed 2218 include wood shakes, slate, tile, composite rubber, and asphalt shingles.

The problem is that typical homeowners’ policies in Canada cover the two types of damage – functional and cosmetic. So even if a hailstorm leaves a roof in working order, the homeowner may file a successful claim to have the roof repaired or replaced strictly because of its appearance.

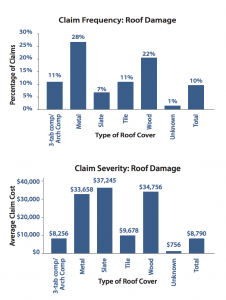

Distribution of claim frequencies with respect to roof covering materials (Claims Analysis Study: May 24, 2011 hailstorms in Dallas-Forth Worth, IBHS)

Needless to say, this adds up, particularly since such roofing products as metal and slate tend to cost considerably more to replace than average asphalt shingles.

As a result of the barrage of large hailstorms that has been affecting such places as southern Alberta in recent years (claims from the 2010, 2012 and 2014 hailers in the Calgary and Airdrie areas together added up to more than $1.7 billion) many insurers have taken to placing separate, larger deductibles on hail-related damage, and some have capped hail-related payouts.

However, such strategies can be unsustainable in the long-run, particularly if competition in the marketplace is intense – as it is with personal property in Canada.

But what if the reduction in coverage is voluntary? What if it is initiated by the insured who, in exchange for knowingly and freely accepting reduced coverage, gets a break on his or her premium and, perhaps, a standard deductible and no cap on payouts?

A number of U.S. states have approved ISO and AAIS endorsements that allow insurers to exclude coverage for property damage caused by wind or hail – that is only cosmetic in nature. In exchange for use of this wording, insureds may get a lower premium (or, at least, may dodge significant premium increases). This wording, it must be underscored, is non-voluntary in nature – if an insured doesn’t want limited coverage, he/she would have to switch to a carrier that doesn’t use the endorsement.

Might it be a consideration to have Canadian personal property writers offer such a wording as an option to insureds that are looking for lower cost insurance? The idea would be akin to an insured removing the comprehensive coverage from an older vehicle in order to save premium.

Is this an idea whose time has come?

Note: By submitting your comments you acknowledge that insBlogs has the right to reproduce, broadcast and publicize those comments or any part thereof in any manner whatsoever. Please note that due to the volume of e-mails we receive, not all comments will be published and those that are published will not be edited. However, all will be carefully read, considered and appreciated.

Leave a Reply