Are personal property insurers asking all the right questions?

1 November 18, 2016 at 3:29 pm by Glenn McGillivray

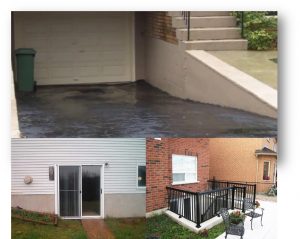

Reverse slope driveways (top), below-grade walkouts (bottom left) and exterior basement stairs often lead to losses during heavy rainfall events that otherwise may not happen.

When an insurance representative makes the decision to bind a new homeowner’s policy, does he/she have all the information needed in order to get a full picture of the risk before it is taken onto the company’s balance sheet?

Said another way, when a rep works with a potential new insured to fill out an u/w questionnaire are all the right questions being asked?

At ICLR, we find that a combination of lab results, post-loss forensic investigations and practical evidence indicates that essentially all homes have risk factors/features that can either cause or worsen a loss. It appears that many of these features are not being considered by insurers in their underwriting questionnaires and, thus, are not factored in when the risk is being priced and the bind/not bind decision is being taken.

And while it is true that some of our findings are state-of-the-science and not yet widely known, there are other more well-established – even obvious – factors that are not being considered when insurance reps bind homeowners’ risks.

Some of the risk factors/features of homes that commonly fail to make it onto underwriting questionnaires include:

Basement flooding/sewer backup (for all homes)

- Does the house have a reverse-slope driveway?

- Does the house have sunken external basement stairs or other below-grade openings?

- Does the house have a below-grade walkout?

- Does the house have window wells and window well covers?

- Have the house’s downspouts been disconnected from the foundation drains?

- Are the house’s foundation drains connected to the sanitary sewer system?

- Does the house have an operable sump pump system and how often does it turn on (give ranges)?

- Does the system include a back-up pump?

- Does the system have a back-up power source?

Wind (for all homes)

- How many stories is the house?

- What type of roof does the house have (flat, gable-end, hip, complex)?

- How steep is the roof?

- How is the house sided (vinyl or other)?

- Does the house have an attached garage and is the garage door single or double width?

- Is the garage door pressure rated or reinforced, if known?

- Does the house have double front entry doors?

Hail (for homes in high-risk hail zones)

- What is the roof covered with (asphalt, clay, metal, slate, wood shakes, other) and how old is it?

- If asphalt, what impact resistance level, if known (Level 1, 2, 3, 4)?

- Does the roof covering have underlayment, if known?

- How is the house sided (aluminum, vinyl, brick, fibreboard, cement board)?

- What type of windows does the house have (single, double or triple tempered glass)?

Wildfire (for homes in the Wildland/Urban Interface)

- What is the roof covered with (asphalt, clay, metal, slate, wood shakes, other)?

- How is the house sided (wood, aluminum, vinyl, brick, fibreboard, cement board)?

- What type of windows does the house have (single, double or triple tempered glass)?

- Does the home have a wooden (or otherwise flammable) porch, deck, balcony, car port etc. attached to it?

- Does the home have a wooden (or otherwise flammable) outbuilding (eg. shed, workshop, detached garage) close to it or a wooden fence close or attached to it?

- Are there trees or shrubs located within 3m of the house?

This list is by no means exhaustive. More questions can be gleaned from ICLR research and communication/outreach materials (much depends on ‘how deep’ an insurer may want to go). Homeowners may not be able to answer a few of these questions, but in some cases the insurance representative could request that the homeowner seek expert advice or provide photos. The rep could also check the home out on Google Earth and Google Street View.

What’s more, if insurers send questionnaires to prospective insureds to have them fill out on their own time, insurers should consider using diagrams and pictures to help describe and explain certain items that may be confusing to insureds, like roof-types and backwater valves (in a May 2011 ICLR survey of homeowners in a flood-prone neighbourhood n London, ON a high proportion of people who were asked if they had a backwater valve responded ‘Don’t know’).

Another issue is that while most (probably all) insurers use underwriting questionnaires when evaluating homeowner risks, many seem to use them more loosely than they would a questionnaire for an auto policy. With auto, usually all questions must be answered and the insured has to sign and date a declaration certifying that all information is accurate. Answering a question untruthfully can lead to cancellation of a policy and/or denial of a claim.

Insurers don’t appear to be quite as forceful with homeowner questionnaires, leaving many questions blank, not asking for follow-up, and not requiring insureds to sign and date a declaration.

Seeing as though profitability of the product has been on the decline in recent years, perhaps It’s time to underwrite homeowner’s insurance more like auto insurance.

The product is no longer the stable, reliable profit-maker that it used to be, and insurers cannot plod on like it still is.

Note: By submitting your comments you acknowledge that insBlogs has the right to reproduce, broadcast and publicize those comments or any part thereof in any manner whatsoever. Please note that due to the volume of e-mails we receive, not all comments will be published and those that are published will not be edited. However, all will be carefully read, considered and appreciated.

We have yet to see insurers take a different approach: It is easy to say what is not right however how is the problem solved. We have not seen insurers spend money in determining what kind of house should be built, with basements, without basements, which roofs are better in different areas of Canada.

In addition, what is the rating system that would handle the fully compliant home( whatever that means) versus those that are partially or not compliant at all. For example higher deductible might be welcomed however the relative premium saving is in a lot of cases negligible and in some cases capped. Or will this become another micro-rating disaster.

Homes can have a number of owners, be of a certain age, have undergone various modifications/renovations.

So now we would request that an owner make representation about his home which might not be aware of nor know. And, if experts would be called in to determine, there would representation ( like home inspections) that would absolve the inspectors of any hidden defects or areas of the home that they could not see.

The subject is very complicated, maybe the solution is multifaceted with everyone being involved, legislators, consumers and insurers.

Maybe just maybe insurer could do inspections.