Could an EF5 tornado hit a major Canadian centre?

0 October 2, 2018 at 4:43 pm by Glenn McGillivray One of the biggest challenges of educating people about natural hazard risk is having to first cut through the myths and misconceptions that envelope essentially every hazard, from earthquake to flood and – yes – tornado.

One of the biggest challenges of educating people about natural hazard risk is having to first cut through the myths and misconceptions that envelope essentially every hazard, from earthquake to flood and – yes – tornado.

Stop me if you’ve heard any of these before:

- Tornadoes can’t happen in cities due to the heat that cities emit

- Tornadoes only happen on hot summer days

- Tornadoes only happen in very specific places

- The sky will turn green just prior to a tornado

- You will always see the vortex

- If you open the windows of a home prior to a tornado, you will equalize the pressure in the home and prevent damage

- While in a car, the best place to be is under an overpass.

There is certainly no shortage of skewed and dangerous misinformation about tornadoes (I’m not even going to get into how people confuse tornadoes and hurricanes!).

But the truth is, we have had tornadoes in Canada in every province, including Prince Edward Island and Newfoundland, and in every month, including January and December. We have had tornadoes in cities (like Regina and Edmonton). We have even had them close to such places as Yellowknife, NWT. And, no, Mother Nature isn’t always so kind as to give advance notice of an impending strike.

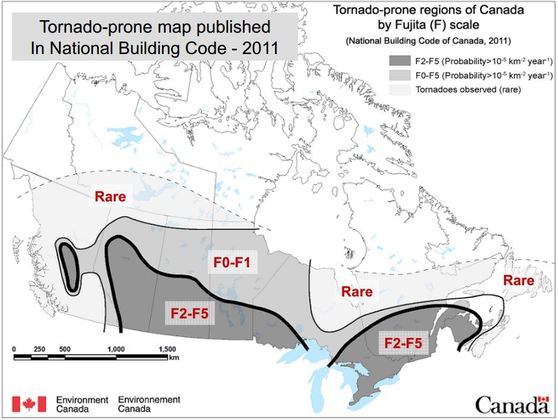

This doesn’t mean that there is equal probability of experiencing a tornado in every province and in every month, as there are clearly peak times of the year when tornadoes are most common and areas of the country where they are more prevalent.

Recent events in the Ottawa/Gatineau region have gotten some in the industry talking about the risk once again (it is not all that often that we see tornadoes ‘get into town’ in Canada. The uncorroborated anecdotal return period for such events, I once heard, is about 10 years). Of particular interest is the fact that one of the six tornadoes that struck the area on September 21 was an EF3*, quite a powerful twister for the time of year (the last F3 to strike in Canada in the month of September was in Merritton, Ontario – now know as St. Catharines – in 1898).

Generally speaking, claims costs from tornadoes in this country tend not to be as high as scenes of the damage may imply. What I mean is that while the carnage may seem very dramatic – even spectacular at times – insured damage has thus far tended to be quite manageable from an industry perspective.

To date, the costliest tornado in modern Canadian history is the July 1987 Edmonton event, which sits at $148.4 million insured (1987 dollars, or $278.1 million 2016 dollars).

More recently, the June 2014 tornado in Angus, Ontario caused insured damage of about $48 million, the August 2011 Goderich, Ontario event caused insured damage of roughly $110 million, and the August 20, 2009 outbreak in Southern Ontario caused insured damage of close to $100 million.

This compares against Canada’s costliest wildfire (about $4 billion insured), its costliest riverine flood (about $1.7 billion), its costliest urban flood (about $1 billion), and its costliest hailstorm (about $570 million).

Spread over several companies and with some reinsurance programs responding, these events aren’t very substantial from an industry perspective, certainly nothing like the 1999 Moore, Oklahoma tornado (USD1 billion insured), the May 2011 Joplin, Missouri tornado (~USD2.16 billion insured) or the 2013 Moore, Oklahoma event (USD2 billion insured).

All three of these tornadoes rated EF5, which leads to the question: Should Canadian insurers be concerned about an EF5 hitting a major centre in Canada?

For a hint, let’s look at the climatology of tornadoes in Canada.

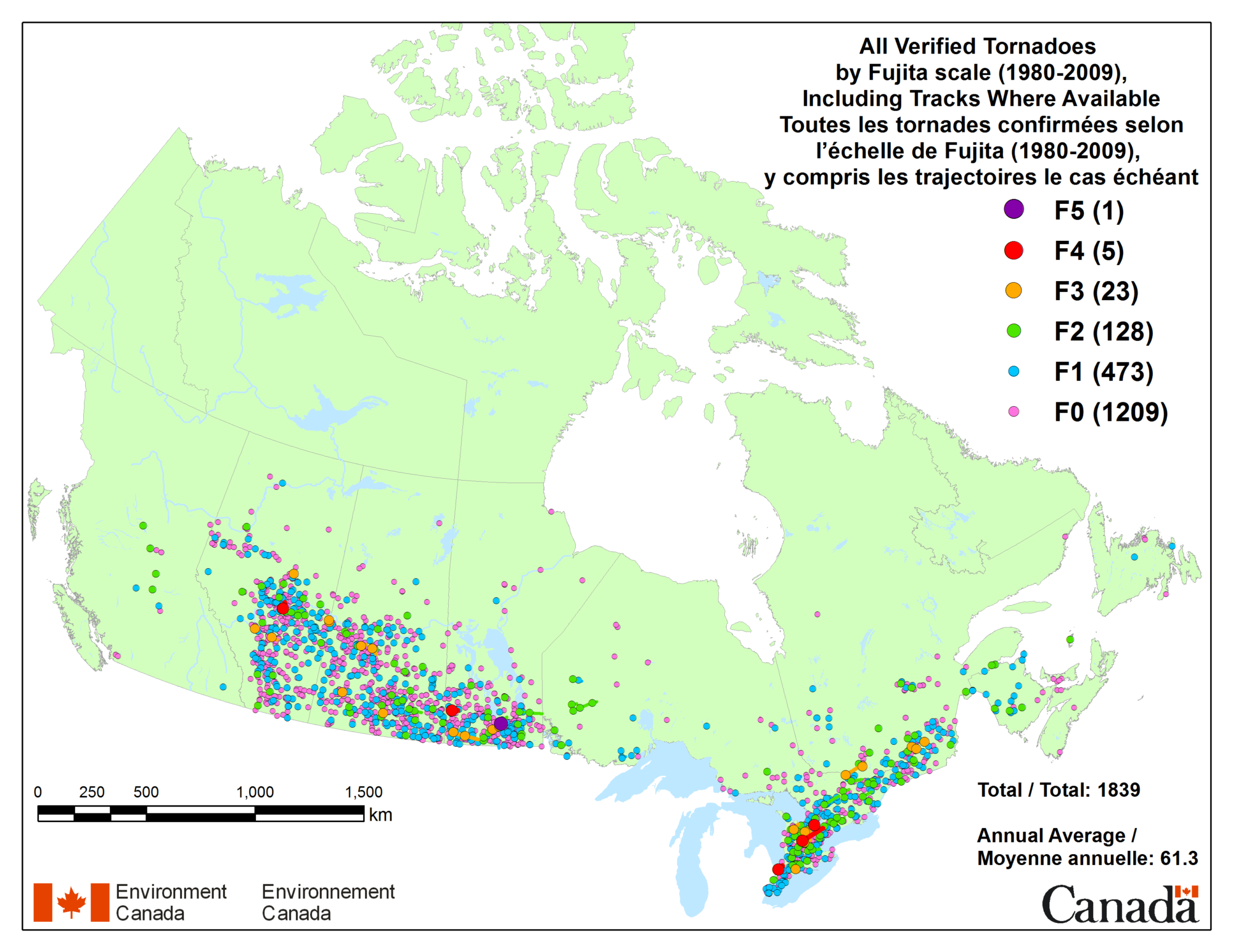

From the period 1980 to 2009, 1,843 tornadoes were recorded in Canada. The breakdown of these are as follows:

F0 or F1

1,217 + 478 = 1,695

91.9% of tornadoes

F2

119

6.5% of tornadoes

F3

24

1.3% of tornadoes

F4

5

0.27% of tornadoes

F5

1

0.0054% of tornadoes

The only F5 ever recorded in Canada occurred in Elie, Manitoba on June 22, 2007. The twister destroyed or damaged several homes, totalled several vehicles, but took no lives. Insured damage came in at about $20.5 million (IBC Facts Book 2018).

According to work conducted by David Sills of Environment and Climate Change Canada, the country likely gets more tornadoes that are actually officially recorded each year (an average of 62), owing for those that occur in remote areas and go unseen. Most of these would likely fall in the EF0 to EF1 range, though it is possible that more powerful tornadoes have occurred but went unreported. Canada, therefore, may have had more than one EF5 in its history, though the probability is quite low.

So should insurers worry about the potential for an EF 5 strike on a major population centre in Canada?

Maybe not (though, of course, they are free to worry if they want to).

Should they be concerned about tornadic storms in major centres at all?

Certainly they should, but not necessarily for EF4s or EF5s (which would be considered as extremely low probability but high to very high impact events).

In my view, insurers should be more concerned about a strike from a well-placed lesser tornado which, statistically, is more likely and which could have fairly serious consequences. Such an event could be of particular concern to a small local/regional writer that may have concentration issues in a given area and a cat reinsurance program that may not be up to the job.

What needs to be reinforced here is that you do not need an EF4 or EF5 to incur total losses of homes and other structures. As was illustrated in Vaughan, Ontario in August 2009 (where two F2s struck, one in Woodbridge and one in Maple) and Angus, Ontario in June 2014 (also an EF2), all you require for a total loss is to lose the roof. When this happens, the home loses it’s structural integrity and must be razed and rebuilt.

Of the roughly 500 homes damaged in the pair of Vaughan tornadoes about 25 had to be bulldozed. In Angus, ten of 100 homes had to be razed due to roof loss. A roof torn from a house is a good as the entire home being wiped from its foundation. There are no degrees of death.

It is important to note that the age of a structure, lack of maintenance and poor building practices can magnify damage (several construction deficiencies were discovered in the Angus homes, for example). Therefore, it is common to get EF3 or EF4 damage from an EF1 or EF2 storm, for example.

Further, an EF2 or EF3 wedge tornado will have a substantially wider damage track than an equal or stronger rope tornado.

So while insurers must always be cognizant of the potential for extremely low probability/high impact events and plan for their eventuality, they cannot and should not lose site of the fact that a lesser event with a higher probability of occurrence but lower impact could, in some circumstances, be almost as painful.

* Up until the 2012 tornado season, Environment Canada used the Fujita Scale to measure tornadoes. It switched to the Enhanced Fujita Scale on April 1, 2013. The new scale is considered to be a more modern and improved version of the original Fujita Scale. The U.S. has been using the EF scale since 2007. The April 18, 2013 tornado in Shelburne, Ontario was the first Canadian twister to be measured under the new system.

Note: By submitting your comments you acknowledge that insBlogs has the right to reproduce, broadcast and publicize those comments or any part thereof in any manner whatsoever. Please note that due to the volume of e-mails we receive, not all comments will be published and those that are published will not be edited. However, all will be carefully read, considered and appreciated.

Leave a Reply