Are insurance customers less loyal? And why?

2 December 15, 2014 at 6:46 am by Christian Bieck

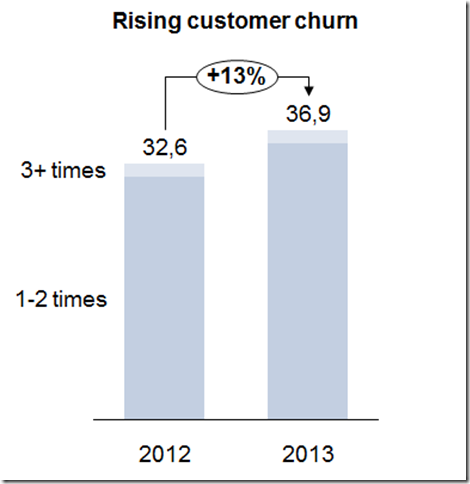

One trend that we have seen of the past few IBV insurance studies that look into consumer behavior (from “Powerful interaction points” through “Insurers, intermediaries and interactions” to “Digital Reinvention for Insurers”) is that insurance customers seem to be becoming less loyal:

The question behind the chart is “How often did you switch your insurance provider in the past two years.” As usual, there is a difference between life and non-life here, but – also as usual – it’s smaller than conventional wisdom would have it (non-life is about 2 percentage points higher, life vice versa. Most of that difference is from motor insurance.)

Eighteen countries went into the comparison, and in 14 of them churn increased. Why? We will be looking into this question into more detail in our upcoming study for next year, but for now, some “informed speculation”.

It’s all about price

Three years ago, I wrote about this statement as one of insurance’s myths. Rechecking again this summer, I think we can safely state that is has stayed a myth – consumers are actually looking for more value, not lower price. Caveat: in some countries, and some parts of the industry, insurers are trying their best to reduce competitive parameters to cost and price. In that case, of course, all else is equal.

Trust matters

Trust in the insurance industry has hovered below 50% ever since the IBV started collecting data on this. Keep up a low trust rate for this long, and it is bound to affect loyalty.

Poor service

Why did our respondents switch? The second most frequent reason given was “poor service” (23.5%). Even assuming that all non-switchers got good service, it means that roughly 9% of our respondents had bad service by their insurers. Might factor into the the low trust from the previous point…

Insurers need to keep up with changing needs

The main reason for their switch given by those 36.9% above was “my needs changed and the previous provider could not meet my new needs” (43.9%). Customer value is strongly driven by understanding customer needs, being prepared for change and being comfortable with it – something insurers are traditionally not very good at.

What do you think are other reasons for increasing churn? And why did churn in the U.S. actually decrease across our two study years (albeit on a very high level)?

Note: By submitting your comments you acknowledge that insBlogs has the right to reproduce, broadcast and publicize those comments or any part thereof in any manner whatsoever. Please note that due to the volume of e-mails we receive, not all comments will be published and those that are published will not be edited. However, all will be carefully read, considered and appreciated.

I would think that in most cases where the customer has indicated that their current provider could no longer meet their needs, it’s a case of the provider not communicating clearly enough what they have to offer. I find that there are a lot of misconceptions about how the insurance industry works among consumers and the industry often is not good at speaking to their audience on a level that they can understand.

Insurers need to stop talking and start listening – and acting on what they hear as opposed to coming up with their own version that suits their purposes. Most customers have pronounced that they want lower rates, yet insurers hear this as “we want more value”. Why do they mis-interpret this? Because they are profit driven. Always up-sell, right? Well in insurance the answer is WRONG. Years ago, insurers added rediculous coverage after rediculous coverage, believing that they could differentiate themselves from their competition, only to find that they could not afford to price the product for the same amount, which then led to coverages being stripped back. Dear customer, we regret to inform you that mold is no longer covered. By the way, no coverage for ice dams unless you pay more. And forget about flood coverage, even though you likely need this more than fire coverage. Personally, after my one and only homeowners claim, I found that my insurer modified their policy the following year to specificially exclude the peril. Nice move.

Insurers need to examine their internal inefficiencies, and understand that investment in the future is the only answer. They cannot be so short sited so as to be blind to what makes businesses successful. Only then will the be positioned to listen to, and meet customer’s needs, as opposed to finding band-aid solutions that will fall off and flounder, never actually meeting the customer’s needs. Give policyholders what they WANT, not what insurers THINK they want or need. And if they can’t get the job done, step aside and get into another industry that doesnt require the same level of expertise.