Insurance Blogs hosted by Canadian Underwriter

Insurance Blogs hosted by Canadian Underwriter

I noticed an interesting section at the end of a recent bulletin issued by FSCO regarding recent regulation changes that I reviewed in a recent post. Thrown in with the announcement of regulatory changes is a discussion on mileage expenses by health care providers.

Read more →Changes will always take place in any industry, but changes in Ontario auto insurance have not solved problems – instead they have created them.

Read more →Several new auto insurance regulations have now been approved by the Ontario Cabinet.

Read more →Uber and similar ride-sharing services aren’t going anywhere. Consumers like these new services and that’s why there are using them.

Read more →The auto insurance focus of this year’s Ontario Economic Statement is consumer protection.

Read more →This week FSCO released rate filings approved for third quarter of 2014. Nine insurers, representing 26.65% of the market based on premium volume, had rates approved in the third quarter of 2014. Approved rates decreased on average by 0.11% when applied across the total market.

Read more →Uber, a San Francisco-based company estimated to be worth $17 billion (U.S.) is aiming to shake up the taxi business in Toronto.

Uber is reported to operate in more than 140 cities in 40 countries around the world, offering taxis, limos and car-sharing services, allowing customers to bypass traditional taxi companies and brokerages to request a ride using their smartphones.

When Uber first set up in Toronto in 2012, city of Toronto officials informed the company that it needed to get a brokerage licence. Uber disputed the request and has been insisting that it is not a taxi service, but rather a technology company, and therefore not subject to licensing requirements. The city has since hit Uber with 35 bylaw infractions and the parties are headed to court. Although, there are some indications that parties are holding discussions.

Hailo, a British company, launched a similar service in 2012 but took a much different approach to Uber. It chose to obtain a brokerage licence. The Hailo app connects customers with taxi drivers, without the need to go through a central dispatch system. This allowed Hailo to be onside with regulators but not with traditional taxi companies who typically charge drivers an average fee of about $600 a month for dispatch services. Hailo is reported to have 2,000 drivers signed up which works out to about 20% of all licensed taxi drivers in the city. Some companies have disciplined drivers for using the Hailo or Uber app.

In London, England, the transport regulator has ruled that Uber be allowed to operate legally until the courts consider a challenge filed by a local taxi drivers’ association. Other jurisdictions are trying to block Uber from operationg. Virginia issued a cease-and-desist order this year and in Pittsburgh, a judge order a halt to operations until the state’s public utility commission has completed a review.

Uber currently operates limo services under UberBLACK and Uber SUV and a taxi service is called UberTAXI. These are traditional services in a sense but use a smartphone app rather than a dispatcher. The drivers carry appropriate auto insurance for a taxi or livery service. The problem arises under UberX which allows ordinary drivers who have been pre-screened to pick up passengers in their own vehicles. Uber claims that drivers undergo criminal background checks and although the vehicles are not mechanically inspected, the do undergo a visual inspection.

The problem with UberX is that their drivers’ personal auto insurance policies are likely invalid while carrying a paying passenger. Uber says it has a $5 million insurance policy that will cover any liabilities that arises while transporting passengers.

In California, state regulators threatened to shut down Uber and other rider-sharing companies over the insurance issue. A deal was finally worked out regarding insurance coverage after a bill was introduced in the state legislature dealing with the issue. The problem gained prominence after an Uber driver struck and killed a 6-year-old girl in San Francisco while on his way to pick up a passenger on New Year’s Eve. Because no passenger was in the car yet, Uber denied responsibility.

In each jurisdiction they operate in, Uber has confronted and won over regulators through a combination of negotiations, hardball tactics and making use of consumer demand for their service. It is only a matter of time before Toronto falls under the Uber spell.

Read more →The Superior Court has upheld an arbitrator’s decision, finding that loss transfer is subject to a two-year rolling limitation period. In Economical v. Zurich, the claimant was driving a car and was involved in a motor vehicle accident with a…

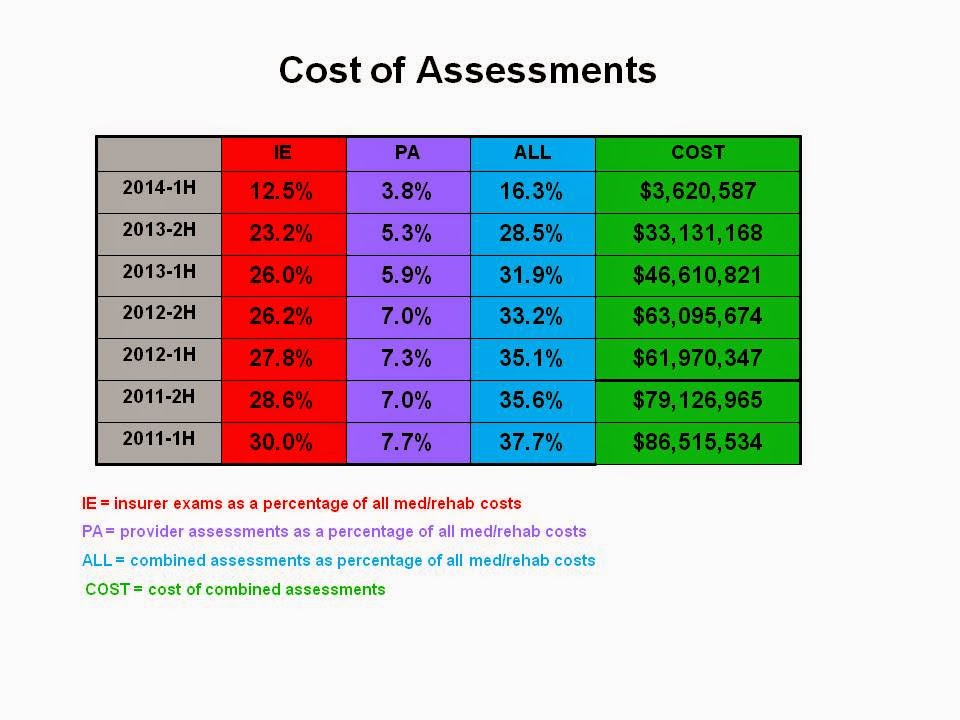

Read more →The IBC has now published the standard HCAI reports for the first half of 2014. The document provides over 75 pages of aggregate data collected by HCAI going back to 2011. HCAI was made mandatory on February 1, 2011.

The standard reports are published on an “accident half year” basis. In accident half year statistics, the experience of all claims with accident dates in the same accident half year is grouped together. The accident half years are defined as calendar half years, with January to June being the first half and July to December being the second half for each of the stated years.

Assessment costs continue to be a significant portion of medical and rehabilitation expenses following the 2010 reforms. Those reforms introduced a $2,000 per assessment cap on both insurer examinations and assessments conducted by healthcare providers. As well, provider assessments now fall under the overall medical and rehabilitation cap.

Based on data from the General Insurance Statistical Agency (GISA), the total cost of all assessments in 2010 was approximately $ 1 billion. In 2010, assessments represented approximately 40% of all medical and rehabilitation expenses.

The chart below sets out insurer exams and provider assessments per accident half year as a percentage of all medical and rehabilitation expenses using available HCAI data. Note that the cost of assessment is not really falling as suggested by the chart. The data is not fully developed and since assessments continue to be a significant cost in older claims, the numbers will continue to grow over time. What is significant is that assessments continue to be close to 40% of all medical and rehabilitation expenses once the data is fully developed.

What has changed is the cost of medical and rehabilitation under the SABS with the reduction in the standard medical and rehabilitation cap and the introduction of the minor injury treatment cap.

HCAI data shows that the majority of claimants see a chiropractor or physiotherapist which is expected since the majority claims are strains and sprains. But as the claims develop, claimants are seeing additional healthcare professionals.

Read more →Although as many as 75% of claims are classified as strains and sprain and should fall under the minor injury definition, only a fraction of those claims receive MIG treatment only. A majority of those claims actually receive treatment within the MIG and additional treatment outside the MIG, likely when the MIG funding is used up. However, that is not to day that they are actually “escaping” the minor injury definition and cap. The average cost of treatment for strains and sprains is under $3,000.

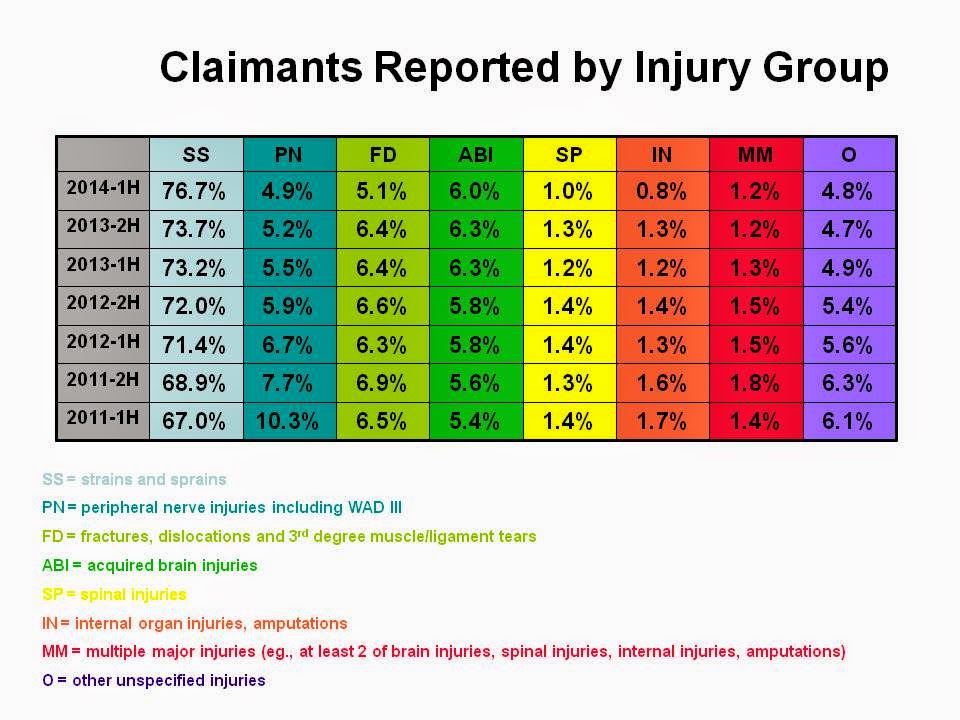

Read more →The IBC has now published the standard HCAI reports for the first half of 2014. The document provides over 75 pages of aggregate data collected by HCAI going back to 2011. HCAI was made mandatory on February 1, 2011.

The standard reports are published on an “accident half year” basis. In accident half year statistics, the experience of all claims with accident dates in the same accident half year is grouped together. The accident half years are defined as calendar half years, with January to June being the first half and July to December being the second half for each of the stated years.

The chart below breaks down the percentage of claimants receiving treatment per injury group. The data is further broken down by accident half year and the percentages are based on claims transactions between the accident date and June 30, 2014.

The injury group sizes have remained consistent since the HCAI began collecting data. The data suggests that there doesn’t appear to be any obvious erosion of the minor injury definition. At least 70% of claimants receiving treatment are being diagnosed under strains and sprains which fall under the minor injury definition. The diagnosis does change over time when you look at previous periods in a chart I posted earlier this year. There has been some drifting from strains and sprains to WAD III (PN) and third degree tears (FD). For example, for the first half of 2013, the SS injury group dropped 2.2% between the two reports while the PN and FD groups increased by 1.0% and 0.8%. This may reflect disputed claims and the time it takes to resolve disputes.

Cars changed the world and our cities in the 20th Century by freeing people of the limitations of their geography. People now have the freedom to live, work, shop and travel almost anywhere they want. The car industry has caused suburbs to grow, and made the development of road and highway systems necessary.

Read more →Some marriages are made in heaven; others are made in Las Vegas. It’s early days yet, but I think the marriage of IBM’s Watson technology with USAA’s insurance and financial services is made in customer service wonderland. If implemented correctly…

Read more →